Ready to send your first bitcoin? That will be $26 please…

Sure, that’s on the high end of what you might pay to use the bitcoin blockchain today, but if you’re new to the world of cryptocurrencies (and haven’t invested that much), we understand seeing such a sky-high sum might be a shock. (Sorry, Kristian!)

Despite what you might have heard about the “money of the future,” the fact is bitcoin (and other cryptocurrencies) are both expensive – and experimental – today.

But while this might not be what you’re used to (or even what you signed up for when purchasing), looking at the reasons behind blockchain costs can help you understand the technology, its weaknesses and where the ecosystem needs more dedicated minds to improve.

OK, so what’s with fees in the first place?

To start, you’re probably thinking this money is all going somewhere. And it is, just not a single place.

When you send a cryptocurrency transaction, you’re paying for it to be included on the protocol’s blockchain, which you can think of as something an official record of every token on the network ever spent (whether it’s bitcoin, ether or something more exotic). Rather than holding this at a bank or a credit card firm, this ledger is distributed.

This means that should any one computer (or group of computers) go down, the network still has a copy showing that you own your asset. The bad news is you have to pay all those computers to process it.

Here, we’ll introduce you to the first new person on our journey, the miner (or validator, depending on your network).

You don’t necessarily know who he or she is, or which one is verifying your transaction – but they are doing work, so to speak, dedicating computing power, putting aside coins or doing some other cost-prohibitive function to help the network to determine which transactions to include in which block of the chain.

For this, they’re rewarded with newly “minted” cryptocurrency.

OK, but why so much?

If that’s confusing, you can think of it like this.

See, every cryptocurrency transaction is made up of a small amount of data, and most blockchains, have limited space for that data as a reference for all those transactions.

In this way, transaction fees represent how interested you are in getting your transaction through, right at that moment, and stored on the network permanently. As you can guess, the bigger the transaction fee – which the miners (or validators) get to collect – the higher your chances are of getting your transaction into the next block that’s processed by miners.

While data limits and how they change vary from blockchain to blockchain (bitcoin has a hardcoded limit of 1 MB per block), in general developers and engineers caution against raising the limit too much, as it can lead to various technical problems.

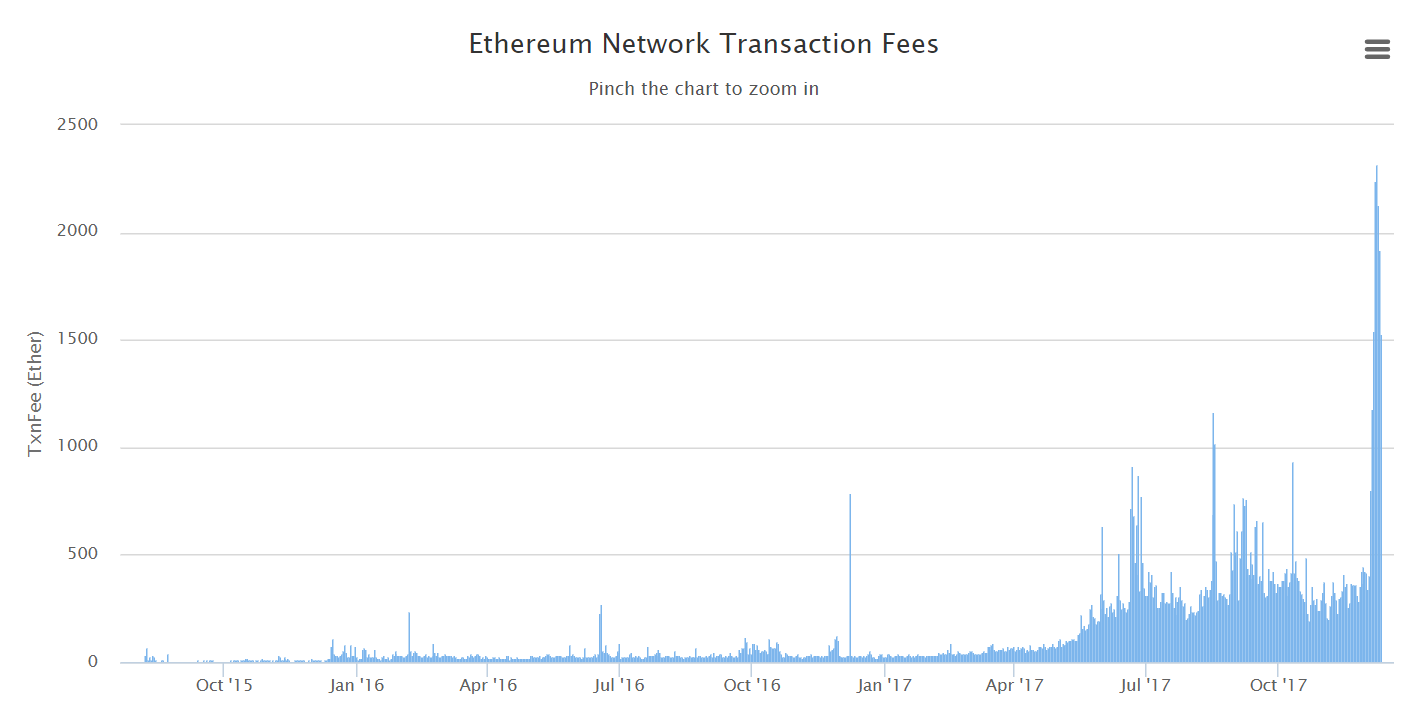

Up until fairly recently, most crypto users didn’t really notice these data limits, since the networks weren’t brushing up against them. But as a new round of crypto investors and enthusiasts hit the market, pushing demand generally up, these data limits are being tested and the associated fees are going up (see chart below).

But what fee should I add?

While it might not seem like it, increasing fees are actually a sign that bitcoin, ether and other cryptocurrencies are growing in popularity and use. But on the other hand, as it’s a fairly recent development, your wallet might not be equipped to make it easy for you.

Ultimately, many wallets (the software that provides the interface with your cryptocurrency) make you decide, giving you the power to determine how much to pay.

Still, transactions without a fee or with too low of a fee during peak usage just sit in limbo.

They’re not outright rejected, but it could take hours, even days, for the network to cool and miners to add the transaction to a block. Plus, as mentioned above, the higher the fee, the more likely it is for your transaction to get picked up by miners.

Deciding what fee is serviceable, though, is tricky.

To help users determine what fee is right, various sites offer calculators, and even some developers have stepped in to try and make that calculation less of a headache.

So, what’s next?

The other option, and arguably the boldest move, is moving into cryptocurrencies that are less-used today.

Yet, the infrastructure around these options may still be limited (bitcoin cash, for example, has fewer merchants than bitcoin), and as such, you should be aware that not only might you have trouble transacting, but development may be ongoing to fix vulnerabilities.

Longer-term, blockchain engineers on many of the largest blockchains are working on a range of “off-chain” solutions that could help the technology scale to more users, all while slashing the cost of using the network, and your transaction fees.

While it’s unclear when these solutions will be ready to deploy on the blockchain for the public’s use, with scaling taking center stage during most technical discussions, many think relief might not take long.